Employee Benefits Insights

Advantages of Partially Self-Funded Health Plans

JUNE 1, 2021

Many employers with fully insured benefit plans share common misconceptions about self-funding. These include: “It’s more work,” “It is too risky,” and “We are concerned about the unknown outcomes.” Or, they don’t fully understand the self-funded approach, and they believe it’s too complicated and would be difficult to manage. At USI Insurance Services, we believe that the advantages of a partially self-funded health plan outweigh the potential drawbacks, and that nearly every employer could better manage its health plan costs on a partially self-funded plan instead of a fully insured plan.

What’s the Difference Between Fully Insured and Self-Funded Plans?

A fully insured health plan is one where the employer pays a fixed monthly premium to the health insurance carrier in return for the carrier paying all plan member claims. If the premium collected is greater than the claims, the carrier retains the excess as profit.

With a partially self-funded health plan, the employer contracts a health insurance carrier or third-party administrator (TPA) to administer all aspects of the health plan, including claims adjudication, but the employer funds the claims payments. Employers purchase stop loss insurance that would pay if any catastrophic claims, such as cancer or premature birth, were to occur. With this arrangement, the employer is paying the health insurance carrier or the TPA considerably less than a fully insured arrangement.

Compared to a fully insured plan, where the employer pays a monthly premium to the carrier that covers the cost of administering the plan and paying the claims, with a self-insured plan, the employer pays less to the carrier or TPA for plan administration, and only pays for the claims processed that month. While claims vary each month, the employer reaps the rewards when few claims need to be paid, and the funds can be set aside in a reserve for future claims.

Statistically speaking, a self-funded plan with at least 100 employees is most likely to save money as compared toa fully insured plan, as demonstrated in this short video. The chart in the video shows that as group size increases, so does the probability that self-funded plans cost less than fully insured plans.

How Do Partially Self-Funded Plans Drive Savings?

The statistical likelihood that partially self-funded plans cost less can be attributed to the following:

- Elimination of carrier profit and premium taxes. Health insurance carriers carefully underwrite their contracts to ensure they will not pay more for a plan than what they’ve collected in premium. In the U.S., individual states impose a tax on insurance premiums that can range anywhere from 0% to 4% of the premium. Removing carrier profit and premium taxes can generate substantial savings in health plan costs.

- Flexibility. Self-funded plans in the U.S. are only subject to ERISA laws and not state health plan regulations and benefits mandates. This affords employers more flexibility to design health plans that are both cost-effective and meet employees’ needs.

- Transparency. Self-funded plans provide greater transparency as employers are able to view claims utilization data, which allows them to make more informed decisions to help reduce costs.

- Competitive bidding. With fully insured plans, the employer’s premium is paying for the plan components, such as claims processing, network access, disease management and pharmacy, all bundled together. Self-funded plans can be unbundled and each component purchased separately, allowing the employer to shop around for the component that best meets its needs and price point.

How Much Can You Save?

For most employers, the combination of the above factors generates total plan savings in the range of 5% to 10% of total plan costs. For an employer with 500 employees, this equates to savings between $250,000 and $500,000 annually. Self-funding also often serves as the gateway to implement additional innovative solutions and strategies that reduce health plan costs, such as reference-based pricing.

How USI Can Help

Our dedicated employee benefits Customer Analytics practice has developed a proprietary Self-Insurance Exploration Analysis tool to help employers determine the savings a partially self-funded plan could deliver. This tool utilizes an employer’s historical data to provide unique insights on the risks and opportunities associated with a self-funded plan, and to help the employer assess its appetite for self-funding.

In addition to the Self-Insurance Exploration Analysis tool, we offer a variety of proprietary solutions to help companies better manage the costs of self-funding. We have negotiated employer-favorable terms and conditions with the leading stop loss carriers to form the USI Stop Loss Consortium, which offers employers best-in-class reinsurance contracts. To help our clients identify top-quality service providers for their benefit plans, USI has created the USI Preferred TPA panel. The TPAs that are a part of the panel have been formally vetted through a comprehensive RFP process to ensure they have the capabilities to deliver quality service to USI clients.

Please contact your local USI benefits consultant if you are interested in the Self-Insurance Exploration Analysis tool to learn how your plan might perform and the potential savings you could see if it were partially self-funded.

COVID-19 Impact on Health Plan Costs at Height of Pandemic

To keep employees safe, employers incurred unexpected expenses for COVID-19 safety protocols, and many also faced significant revenue losses due to the economic downturn. However, stay-at-home orders caused fewer doctor visits and many canceled surgeries, which led to a drop in utilization at the height of the pandemic in 2020. As a result, there were significantly fewer claims to be paid.

To keep employees safe, employers incurred unexpected expenses for COVID-19 safety protocols, and many also faced significant revenue losses due to the economic downturn. However, stay-at-home orders caused fewer doctor visits and many canceled surgeries, which led to a drop in utilization at the height of the pandemic in 2020. As a result, there were significantly fewer claims to be paid.

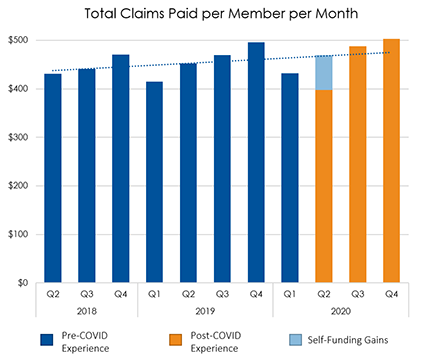

USI performed an analysis of our entire book of self-funded clients to determine the impact of the COVID-19 pandemic. A trendline was plotted using data from the months prior to the pandemic, and while Q3 and Q4 of 2020 fell within the trended expectations, there was a significant drop in claims for Q2. This resulted in an average savings of $72 for our clients for April, May, and June of 2020. These savings translated to $18 per member per month (PMPM) spread across the course of 2020, or 3% to 4% of total plan costs. For an employer with 500 employees, this equated to savings of $150,000 to $200,000.

Employers with fully insured plans experienced the same drop in utilization in Q2 of 2020, but they continued to pay the same premiums to their health insurance carriers. USI estimates these fully insured employers overpaid their premiums by $25 to $75 PMPM. For an employer with 500 employees, this equated to $78,750 to $236,250 in premium overpayments. Unfortunately, the lower utilization in 2020 rarely resulted in lower 2021 premiums for fully insured clients, as insurers increased premiums due to forecasted raises in costs for deferred care, COVID-19 testing and treatment, and vaccination costs.

While the pandemic has delivered numerous unprecedented challenges to all employers, those with partially self-funded plans saw a boost in cash flow that was beneficial to their business operations. Employers with fully insured plans received no such boost despite experiencing the same drop in utilization, and many had to cut costs elsewhere in their businesses.

SUBSCRIBE

Get USI insights delivered to your inbox monthly.