Emerging Business Insights

Control Auto Insurance Costs With Accurate Classifications

MAY 5, 2026

As companies grow, they’re often not thinking about things like updating insurance information, including their vehicle list — leading to unnecessarily high premiums. Errors related to vehicle classifications can cause you to pay more in premium each year, but this can easily be avoided.

How Classifications Can Affect Premium Costs

Accurate automobile classifications are instrumental to getting the lowest premium. Rating factors include vehicle weight, vehicle usage, radius of use, and garaging. Correcting the most common mistakes on any of these factors can result in premiums savings of up to 35%.

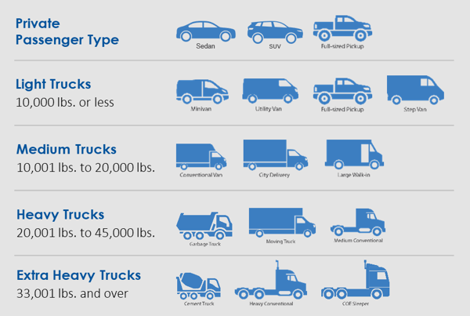

Gross Vehicle Weight and Classification

Insurance companies use a classification system to categorize vehicles based on gross vehicle weight. Heavier vehicles are charged higher rates due to their potential to cause greater damage.

Because underwriters rely on applications from insurance agents, inaccurate information could be carried across multiple policy terms. Liability and physical damage rates generally increase with higher gross vehicle weight; inaccurate classification can inflate premiums by up to 30%.

Business Use Classification

Usage classifications are based on how vehicles are normally used. If a vehicle has more than one use, the highest rated classification is usually picked by the insurance company and can impact premiums by up to 35%.

- Service Use: Vehicles used to transport workers or supplies to and from job sites; parked most of the time.

- Retail Use: Vehicles used for pickup or deliveries to individual households. They’re on the road most of the time and frequently change routes. Rates can vary by up to 35% over Service Use.

- Commercial Use: All other vehicles besides Service Use or Retail Use. Rates can vary by up to 20% over Service Use.

Vehicle Usage Example

USI Insurance Services worked with an HVAC contractor that had 7 work trucks. After reviewing their operations, it was determined that 3 of the vehicles were misclassified and had been rolled over through several renewal cycles by their current broker.

Three of the 7 vehicles were misclassified as retail use and the other 4 were correctly classified as service use.

The contractor and USI agreed on how the vehicles should be classified. By re-classifying the three vehicles properly as Commercial use, the average premium cost per truck was lowered by 14%.

Radius of Use

Distance typically traveled by a vehicle impacts premium — the shorter the distance traveled, the less expensive the premium. Radius is measured in a straight line from the principal place of garaging. This is particularly important for transportation/trucking companies.

- Local: Up to 50 miles from principal garaging location

- Intermediate: 51 to 200 miles from principal garaging location. Rates are typically 5% to 10% higher than Local.

- Long Distance: More than 200 miles from principal garaging location. Rates are typically 10% to 20% higher than Local.

Radius Example

A distributor with a fleet of 9 trucks was concerned that their auto insurance costs were too high.

USI evaluated their operations and determined only 4 of their trucks were used for long distance, but all 9 were being classified as long distance. Making matters worse, that information had been rolled over through several renewal cycles by their current broker.

USI worked with the insurance company to correct the classifications and saved the distributor 15% on its premium.

Territory & Location (Garaging)

The location where vehicles are garaged influences the premium. Insurance companies typically base rates on territory or zip code, and premium may vary up to 20%.

- Factors such as traffic and crime determine how the cost of coverage differs between rating areas.

- Rates are usually higher in urban areas due to the number of hazards that can lead to auto claims.

- Understanding how garaging impacts premium allows businesses to make informed decisions as to where to store their vehicles.

Bottom line: Make sure that classifications are represented accurately, so the insurance company can determine a fair premium charge at the inception of the policy term.

How USI Can Help

USI conducts comprehensive reviews of automobile classifications to help businesses provide more accurate underwriting data to insurance companies and gain more control over premium. Correcting misclassifications that other brokers roll over from prior policy years allows us to deliver significant cost savings to businesses.

We evaluate vehicle classifications to determine the most accurate and cost-efficient codes by:

- Gathering information on company operations and current exposures, and comparing them to those assigned on the policy to discover potential mistakes or discrepancies.

- Amending classifications and exposures appropriately.

- Exploring the possibilities of recovering premiums from prior years.

In addition to the exposures discussed in this article, USI’s analysis of automobile insurance programs can identify other opportunities to reduce uninsured exposures and create premium savings. To learn more about the risk management services available through USI, email select.business@usi.com.

SUBSCRIBE

Get USI insights delivered to your inbox monthly.