Emerging Business Insights

Control Your Experience Mod to Reduce Workers’ Comp Premiums

NOVEMBER 1, 2022

A business’s workers’ compensation experience modification factor, or experience mod, has a direct correlation with insurance premium costs. The experience mod is an indicator of the business’s loss history compared to its industry peers', and is used as a multiplier to either increase or decrease premium.

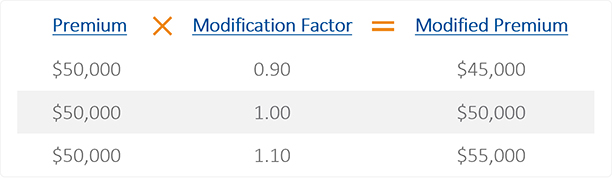

- An experience mod of 1.00 is reflective of average losses, and does not affect the premium.

- An experience mod lower than 1.00 represents better-than-average losses, and produces a credit against the premium.

- An experience mod higher than 1.00 represents worse-than-average losses, and produces a debit against the premium.

Job classifications, payroll and claims are the key components used to determine experience mod. An error in any one of these can result in a higher premium. USI Insurance Services conducts detailed experience mod reviews for clients to help them better understand how these components impact their premiums. We also identify what type of injuries are driving the claims, so safety protocols can be developed and implemented. Armed with this information, businesses can gain control over their experience mod and potentially reduce premiums by 5% to 20%.

Many businesses believe that simply having an experience mod below 1.00 is the goal. But knowing how low it can be is important. The difference between the current experience mod and the minimum mod, a number unique to each business, represents the opportunity for further savings.

Although the process is complex, USI’s analysis can provide you an edge over your competitors and ultimately lower your total cost of risk.

Example

A general contractor was having a tough time qualifying for new work because their workers’ compensation experience mod was 1.13, which was higher than what was required by some of the contracts on which they wanted to bid.

When we verified their historical payroll amounts by worker classification and evaluated their open claims, we identified payroll errors and a claim reserve that was set too high. After pointing this error out and advocating on behalf of the contractor with the insurance company, we were able to reduce the experience mod from 1.13 to 0.98, creating a premium savings of almost $7,800. The reduced experience modification rating also allowed the contractor to bid on and win several new contracts worth over $4,300,000.

Having your experience mod analysis conducted by a broker with expertise in your industry presents the opportunity to:

- Confirm the experience mod calculation is correct

- Identify the key claims driving the current experience mod

- Determine the minimum experience mod

- Help develop a plan to improve the experience mod

USI’s better and different approach to properly perform this analysis can save our clients up to 20% on their workers’ compensation premiums.

How USI Can Help

USI works with insureds to do the following:

- Analyze payroll, class codes and loss information for the past three years

- Review and correct the current experience mod, which impacts premium

- Determine the financial impact of any standout claims and project future savings opportunities

To learn more about the experience mod review services available through USI, email select.business@usi.com.

SUBSCRIBE

Get USI insights delivered to your inbox monthly.